|

|

Introduced in the early nineties, the balanced scorecard actually had roots going back about a century when some companies began systematically analyzing non-financial data as part of their performance assessment. More recently, a model had emerged that included four dimensions:

- Customer

- Financial

- Internal

- Learning and Growth

The customer dimension focused on gaining and retaining customers through quality and service objectives. The financial dimension was composed mainly of traditional historical financial goals and measures, directed at bottom line performance. The internal dimension zeroed in on the critical components of internal operations that would make success in the customer and financial perspectives possible. The learning and growth dimension measured the elements of the organization that would dictate future sustainability, such as employee skills and research and development. Objectives for the internal dimension were often derived from looking at the other three perspectives and determining what gaps existed in the organization, in terms of skills and innovation.

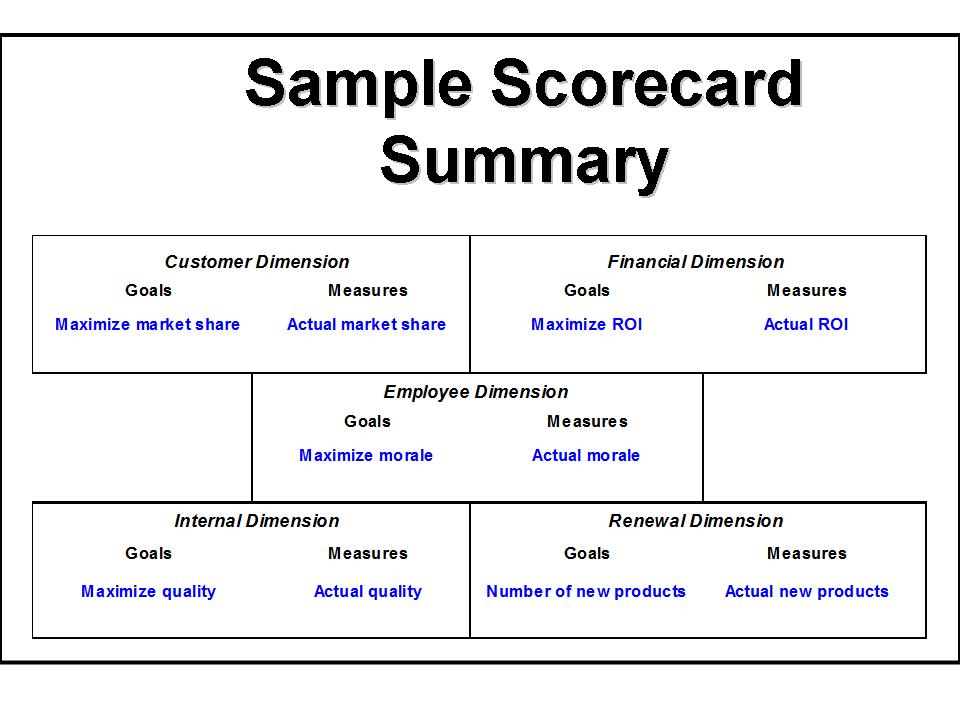

One method of creating the scorecard is to first complete a balanced scorecard summary (see diagram below), which includes the goals and measures for each dimension. Each dimension can be weighted to indicate its relative importance.

The next major step is to then add the necessary detail to each dimension, including weights (if desired), targets and stretch targets necessary for each goal. This facilitates scoring on three levels: by goal, by dimension, and on the overall scorecard. Armed with this information, the organization is able to gain a strong sense of performance against expectations on all levels.

The information in this section was referenced from: R. Kaplan and D. Norton, "The Balanced Scorecard: Translating Strategy into Action", (Boston: Harvard Business School Press, 1996)

CLICK HERE TO VIEW OUR WORKSHOP INFORMATION

HOME | SERVICES | TESTIMONIALS | PUBLICATIONS | STRATEGY MAPPING | THE BALANCED SCORECARD | RISK MANAGEMENT | ABOUT US | CONTACT US

Property of AMI Incorporation, 2006 |

Designed by ellips design + consulting